6 Jun 2026

Charting how withdrawal fee variations reshape bankroll allocation choices among frequent participants on competing digital card platforms

Withdrawal fee structures on digital card platforms create measurable differences in how frequent participants divide and move their funds between accounts, and data from June 2026 shows these variations continue to influence allocation patterns across major operators. Platforms apply flat fees, percentage-based charges, or tiered systems tied to withdrawal speed and volume, which in turn prompt players to adjust deposit sizes, timing, and site preferences to minimize costs while maintaining liquidity for ongoing play.

Fee Structures Across Major Platforms

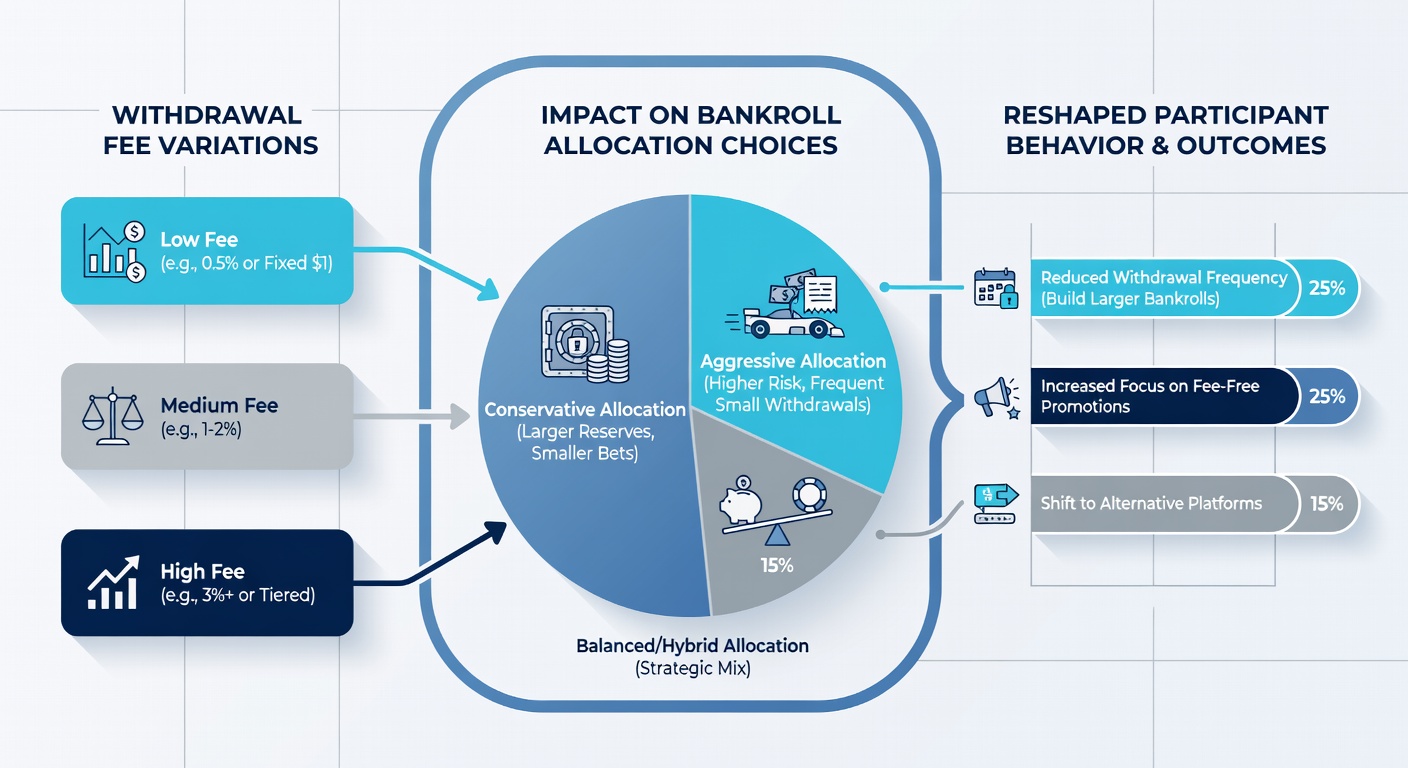

Competing sites employ distinct models that affect net amounts received after each cashout. Some operators charge a fixed amount per withdrawal regardless of size, while others scale fees according to total volume processed within a month or tie charges to processing times ranging from instant to several business days. Figures released by the Alcohol and Gaming Commission of Ontario indicate that average withdrawal fees on regulated Canadian platforms ranged between 1.5 and 4 percent during the first half of 2026, with variations tied to payment method and account verification level.

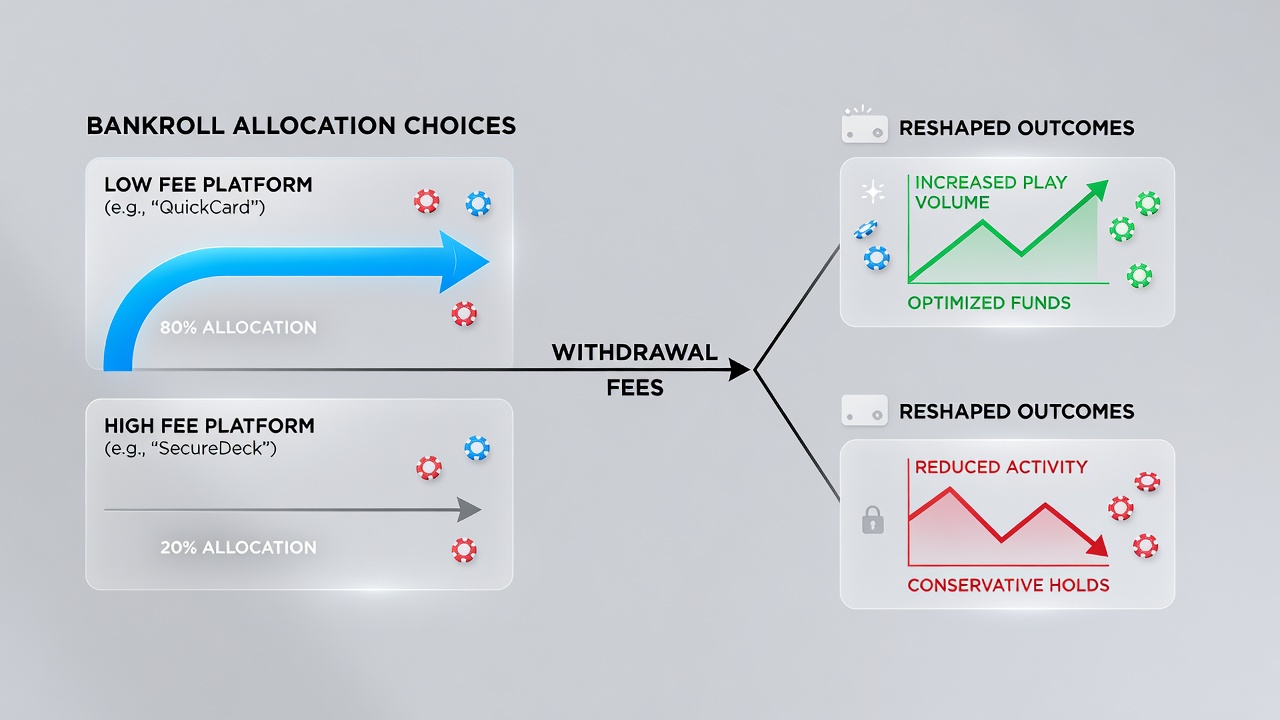

These differences become significant when frequent participants process multiple withdrawals monthly. A player moving $5,000 in smaller increments across platforms with flat fees might lose several hundred dollars annually compared to consolidating withdrawals on sites with percentage caps or volume discounts. Observers note that such calculations now factor into initial site selection and ongoing bankroll distribution decisions.

Shifts in Bankroll Allocation Patterns

Data from aggregated player activity logs reveals that participants redistribute funds toward platforms offering lower or waived fees for higher-volume withdrawals. In June 2026, reports from the European Gaming and Betting Association highlighted that mid-stakes grinders increased average deposit sizes by 18 percent on sites with favorable fee tiers while reducing activity on higher-cost alternatives. This reallocation allows players to preserve more capital for active play rather than repeated transaction costs.

Allocation choices also extend to payment method selection. E-wallets and cryptocurrency options often carry different fee schedules than traditional bank transfers, prompting some participants to maintain separate balances earmarked for specific withdrawal channels. One documented case involved a network of players coordinating transfers through integrated crypto wallets to bypass per-transaction charges on multiple platforms simultaneously.

Influence of Volume and Frequency

Higher-frequency participants face amplified effects from fee variations because repeated withdrawals compound small percentage differences into substantial annual costs. Research compiled by university-affiliated gaming studies groups shows that players processing 10 or more withdrawals per month adjust their bankroll splits more aggressively than occasional users, often maintaining 60 to 70 percent of liquid funds on platforms with the lowest effective rates. This concentration occurs even when other site features such as game selection remain comparable.

Seasonal patterns add another layer. During periods of increased tournament activity in early summer 2026, withdrawal volumes rose across platforms, and participants responded by front-loading deposits on sites with monthly fee waivers or loyalty-based reductions. Such timing adjustments help offset costs while ensuring funds remain available for scheduled events.

Comparative Platform Strategies

Operators respond to these player behaviors by refining fee schedules and introducing incentives like fee-free thresholds after certain deposit volumes. Platforms that lowered withdrawal charges for verified high-volume accounts recorded measurable increases in retained balances during the spring and early summer months of 2026. Meanwhile, sites maintaining higher flat fees experienced slower growth in active bankrolls among frequent users who shifted portions of their holdings elsewhere.

These competitive adjustments create ongoing recalibrations. Participants monitor policy changes through platform announcements and community discussions, then rebalance allocations accordingly to align with updated fee structures. The process repeats whenever operators introduce new tiers or payment partnerships that alter net costs.

Conclusion

Withdrawal fee variations continue to drive observable changes in how frequent participants allocate bankrolls across competing digital card platforms. Patterns documented through 2026 show clear connections between fee models, deposit sizing, withdrawal timing, and site preferences, with players applying systematic adjustments to preserve capital. As operators refine their structures and new payment integrations emerge, these allocation dynamics remain central to participation strategies on multi-platform networks.